Out-of-the-box thinkers… that’s one way to describe those of us who spend all or most of our time living and working in our RVs. We enjoy the freedom and adventure of living on the road, but it does come with some challenges—for example, we generally face a more complicated tax situation and are driven (pun intended) to focus our creative abilities on the task of minimizing our tax burden.

Earning a living while traveling through multiple states (and countries) could awaken tax enforcers who might come knocking on our thin metal doors seeking remittance for their coffers. We want to make sure we’ve done our homework and avoid paying more tax than legally required.

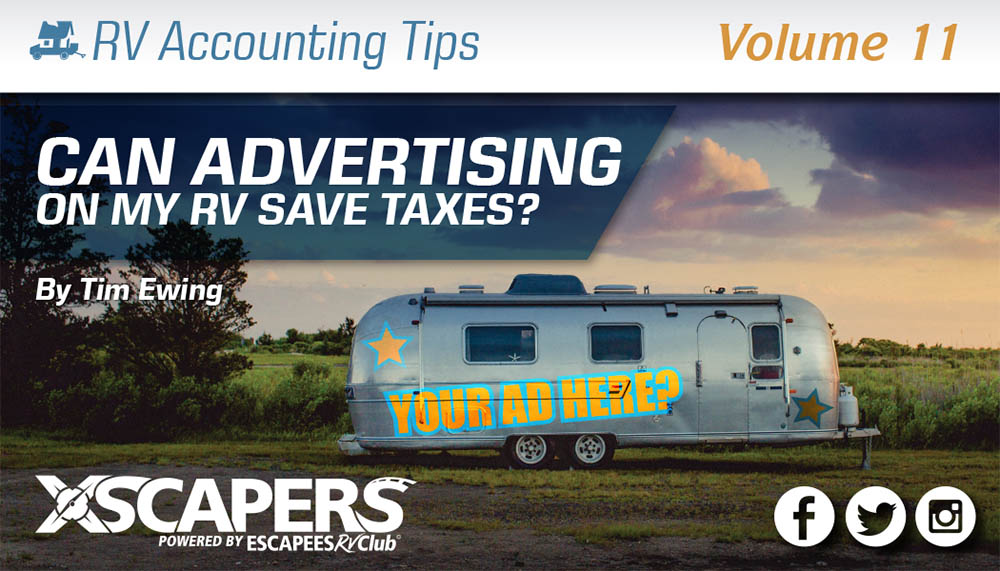

One of the more creative tax saving ideas put forth by my fellow RV nomads involves converting an RV into a mobile advertisement for a business. Could it be that simple, all we need to do is add some promotional signage to the exterior of our rig, or perhaps cover it bumper to bumper with a custom wrap? Could advertising convert otherwise non-deductible RV expenses into legitimate tax deductions? Let’s examine what the IRS says.

Deductions allowed and not allowed

The IRS does acknowledge that advertising and promotional expenses are legitimate business activities and deductible for income tax purposes. Specifically, the IRS instructs, “You generally can deduct reasonable advertising expenses that are directly related to your business activities.” (1) Certainly, it is reasonable to deduct the expense to create an ad regardless of whether it will appear on a webpage, in a magazine or on a roadside billboard. But does that same logic carry to an ad placed on the exterior of a vehicle or trailer? Yes, it does. But before we get too excited, we need to differentiate between the cost of creating the ad and in the case of our RVs, the cost to transport our mobile “billboard”.

As noted above, the IRS allows a tax deduction for costs involved in creating an ad, regardless of where you use the ad, including the exterior of an RV. These costs include design work, materials, purchased labor and related services necessary to adorn your rig with your business advertisement. Unfortunately, the IRS disallows a deduction for other RV-related expenses (e.g. travel expenses) even though the RV is now a mobile advertisement. In other words, the ad does not change your use of the RV from personal to business, even if you wrap your entire RV in a giant advertisement.

In IRS Publication 463 we find that, “Putting display material that advertises your business on your car doesn’t change the use of your car from personal use to business use. If you use this car for commuting or other personal uses, you still can’t deduct your expenses for those uses.” (2)

For income-earning RVers whose only residence is their RV, the IRS confers the status of “itinerant”. This means travel in the RV can never be a deductible business event, it is always personal—even if your rig is wrapped in advertising. RVers who have a separate residence from their RV may already be able to deduct certain travel expenses so adding exterior advertising would not be a factor in determining what travel expenses may or may not be deductible. (3)

What if the business owns the RV?

Does it make a difference if the business owns the RV instead of an individual? Unfortunately, no. Ownership does not change how the IRS defines the deductibility of expenses. Regardless of who owns the RV, the IRS looks at what percent of its use is business versus personal. For itinerants, RV travel is always defined as personal even if the RV is business-owned. (4)

Be sure to connect with a CPA if you have any out-of-the-box ideas for tax deductions (some of them could be useful) or need help wrestling with your tax situation.

(4) Personal use of a business asset opens up another Pandora’s Box of tax complications so be careful about strategies that involve business ownership of your RV.

DISCLAIMER: The information and materials we share in this article are intended for reference only. As the information is designed solely to provide guidance to the readers, it is not intended to be a substitute for someone seeking personalized professional advice based on specific factual situations. Therefore, we strongly encourage you to seek the advice of a professional to help you with your specific needs.

Author

Tim Ewing - Certified Public Accountant (CPA)

Tim began the RV life in 2014. For over 30 years, he has provided tax and CFO services for small businesses and non-profits and currently operates his CPA practice full-time while on the road. Tim specializes in helping self-employed RVers unload their bookkeeping burdens and avoid IRS headaches. You can reach Tim at timewing@quest-cpa.com or by phone 757-771-2557.

Previous Post

Previous Post Next Post

Next Post