Healthcare Options for Pre-Medicare RVers Part 1

Navigating the complexities of the healthcare system on the road is a challenge for all RVers, but it’s downright daunting for those who are too young to be eligible for the only true nationwide healthcare plan—Medicare—available in this country. When my wife and I became full-time RVers in our mid-50s, we had to research this topic for ourselves. Since then, I’ve given several live presentations and webinars to share what I’ve learned about healthcare options for pre-Medicare RVers with other Escapees members.

In this first in a series of blog posts, I’ll explain some important concepts that are fundamental to understanding healthcare coverage. In future installments, I’ll review the different types of healthcare options available to pre-Medicare RVers, delve into Affordable Care Act (“ACA” or “Obamacare”) marketplace plans, explore subsidies under the ACA, and provide some suggestions on how to choose among the various available alternatives.

What is the purpose of healthcare coverage?

Contrary to what some people think, the purpose of healthcare coverage is not to defray your routine medical expenses. I often hear people who are in their twenties and thirties say, “I’m young, I’m healthy, I don’t take any prescription medications, I don’t have any chronic illnesses—so I don’t need to worry about healthcare coverage.”

But nothing could be further from the truth.

The purpose of healthcare coverage is to cover unexpected and potentially catastrophic expenses. The key words there are unexpected and catastrophic, meaning severe illnesses (think cancer, stroke, or heart attack) or traumatic injuries (like from an auto or bicycle accident) that you can’t foresee and that can hit anyone, regardless of your health or your age.

Going without healthcare coverage creates two big risks for pre-Medicare RVers. First, some healthcare providers—particularly specialists and hospitals—may refuse to treat you if you can’t prove financial ability to pay the bill. Although policies vary, you really don’t want to take that chance. Second is the risk of a life-altering financial disaster. Nearly 60% of people who filed for bankruptcy said medical expenses “very much” or “somewhat” contributed to their bankruptcy—more than the number who cited home foreclosures or student loans. Why gamble with your hard-won freedom to travel?

Understanding Nationwide Access

People who live in one place generally never worry about access to healthcare providers outside their home state. They get their routine care when they’re home, and most health insurance policies cover true emergencies—even out of their provider network—when away from home.

RVers, on the other hand, travel extensively. For that reason, it becomes critical to know if we have coverage and access to our insurer’s provider network outside of our home state. (Most healthcare policies provide limited or even no benefits when you use an out-of-network provider, other than in an emergency.)

This can be difficult to determine from the information that insurers and other organizations provide. Look in their literature for a statement like “this plan provides access to a nationwide provider network.” If you’re not sure, it’s best to call them and ask, “if I need to see a doctor for a routine thing like a sore throat and I’m not in my home state, am I still covered, and is there still a provider network outside the state?”

Also, look at whether your plan is an HMO (health maintenance organization) or a PPO or EPO (preferred or exclusive provider organization). HMOs require that you see your primary care physician (PCP) before you can visit any kind of specialist. Of course, your PCP will be in your home state, which makes it impractical if you’re out of state and need specialty care. In addition, most HMOs provide no coverage at all outside your home state, except in a true emergency.

Domicile

If you’re a full-timer or even a part-timer, you’re probably already familiar with the concept of domicile. As it relates to healthcare, you can get coverage only in the zip code of your domicile. The cost of healthcare coverage and the availability of suitable plans can vary greatly from state to state, and even from one zip code to another within a given state. For many pre-Medicare RVers, this is a key driver in choosing their domicile. In some cases, the cost and availability of healthcare coverage may even make it worthwhile to change domiciles, as we did in 2017, from Texas to Florida. (Escapees has an in-depth guide to domicile, which is a complex topic itself.)

Affordable Care Act

The Patient Protection and Affordable Care Act of 2010, more colloquially known as the Affordable Care Act, ACA, or Obamacare, is much more than just subsidies for low- and middle-income people. It provides numerous protections for consumers who subscribe to plans that comply with the requirements of the law. The downside of the ACA is that it caused somewhat higher premiums for traditional medical insurance. This happened both because the ACA requires a broad range of benefits, which increases costs to insurers, and because of the political uncertainty that has swirled around the ACA for the last several years, which increases insurers’ financial risk—which they pass along to consumers in the form of higher premiums.

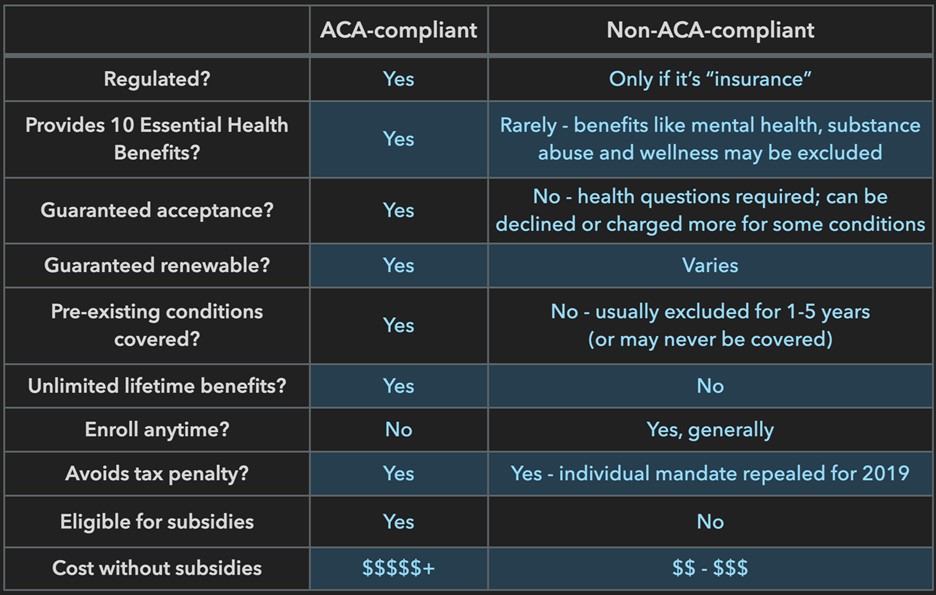

The universe of healthcare coverage options can be divided into two distinct types of plans: those that comply with the provisions of the ACA, and those that don’t. As a consumer, it’s vital to understand the differences in what you’re getting between ACA-compliant and non-compliant plans. The chart below summarizes some of the key differences.

Regulation

ACA-compliant plans are regulated by federal law and sometimes by state law as well. In contrast, non-ACA-compliant plans may or may not be regulated, depending on whether they fall within the definition of “insurance” under each state’s laws. Regulation—at either the federal or state level—provides numerous protections for you as a consumer, including standardized disclosure requirements, anti-fraud rules, financial solvency requirements, and a means of investigation of complaints and enforcement of the laws, usually by a state insurance board. Most of these protections don’t exist if a plan isn’t regulated.

Essential Health Benefits

All ACA-compliant plans must provide coverage for the 10 essential health benefits shown in the graphic below. But non-compliant plans almost always provide more limited coverage—often omitting benefits like mental health, substance abuse services, maternity, and newborn care, or even prescription drug coverage—to keep premium costs lower. When you purchase a non-compliant plan, the responsibility is on you to understand exactly what is and is not covered.

Guaranteed acceptance

You cannot be denied coverage or charged a higher premium for an ACA-compliant plan due to your health history. In contrast, non-compliant plans will almost always use some form of underwriting, in which they ask questions about your health history and current conditions. Based on your answers, non-compliant plans may decide to either not cover you or charge you more.

Guaranteed renewability

ACA-compliant plans are always renewable, meaning that at the end of the plan term, you can renew that plan for another year, even if your health has deteriorated. Non-compliant plans don’t have this guarantee. Some (especially short-term medical plans) may require you to repeat the underwriting process before each renewal. to prove that you’re still insurable. Other non-compliant plans may outright decline to renew your policy based on your claims experience with them—forcing you to find other coverage.

Coverage for pre-existing conditions

ACA-compliant plans are not permitted to exclude coverage for any pre-existing conditions you may have. Non-compliant plans, on the other hand, almost always exclude most or all conditions for which you’ve received a diagnosis or been treated within the previous several years. Sometimes these exclusions are removed after some period, but in other cases, no coverage for them will ever be available.

Unlimited lifetime benefits

ACA-compliant plans must have no cap on the benefits you can receive under the plan during a year or your entire lifetime. But non-compliant plans almost always do cap your benefits—often to somewhere between $1 million and $3 million. Limiting their maximum risk allows these plans to offer lower premiums. Those lower premiums may look attractive today, but remember: you’re getting this coverage to protect yourself against catastrophic financial loss. With today’s medical costs, it’s easy for the bill for a major injury or serious illness to run into the millions of dollars in a matter of weeks. You want your insurance to pay all of that bill, not just part of it!

Enrollment window

One advantage of most non-ACA-compliant plans is that you can enroll in the plan at any time during the year. On ACA-compliant plans, however, there’s only a short period of time each year—sometimes as little as six weeks—during which you can enroll. (This “enrollment window” exists because otherwise, you could simply wait until you get sick and then sign up for insurance. That would mean that only sick people would have insurance, causing premiums to skyrocket even higher than they have been.)

There are two types of enrollment windows for ACA-compliant plans: “open enrollment”, which is a set period each year when anyone can enroll, and “special enrollment periods”, which last for 60 days from the time that you have a qualifying life event. “Qualifying life events” include things that don’t happen frequently, like marriage or having or adopting a child, but—important for us as RVers—they also include moving to a new domicile. Involuntary loss of other healthcare coverage—such as due to involuntary termination from your job, divorce if you’re on your spouse’s policy, COBRA expiration, or aging off a parent’s plan—is also a qualifying life event that entitles you to a special enrollment period.

Tax penalties

When the ACA took effect, there was a small penalty—formally known as the “individual mandate”—payable on your income tax return if you failed to enroll in an ACA-compliant plan. However, Congress repealed the individual mandate in 2019, so it is no longer an issue even for non-compliant plans.

Eligibility for federal subsidies

ACA-compliant plans are eligible for federal subsidies—officially known as the Premium Tax Credit—which can offset a huge amount of your premium, sometimes even reducing it to zero. Non-ACA-compliant plans are not eligible for subsidies. For this reason, it’s critical to determine if your income and family size will qualify you for a subsidy. Be aware that the American Rescue Plan of 2021 dramatically increased the income limits for subsidies in 2021 and 2022. If you’re eligible for a subsidy, you definitely will want to get onto an ACA-compliant plan on the federal marketplace or your state marketplace.

Cost

Of course, the other major downside to ACA-compliant plans is that they are usually very expensive if you’re not eligible for a subsidy. As I’ve pointed out above, non-compliant plans usually cost less than their unsubsidized ACA-compliant counterparts because they offer significantly more limited benefits.

Next in Healthcare Options for Pre-Medicare RVers

Now that we’ve covered some of the basic concepts of healthcare options for pre-Medicare RVers, in the next post in this series, we’ll survey the various options—both ACA-compliant and non-compliant—that are available to us as RVers.

Previous Post

Previous Post Next Post

Next Post